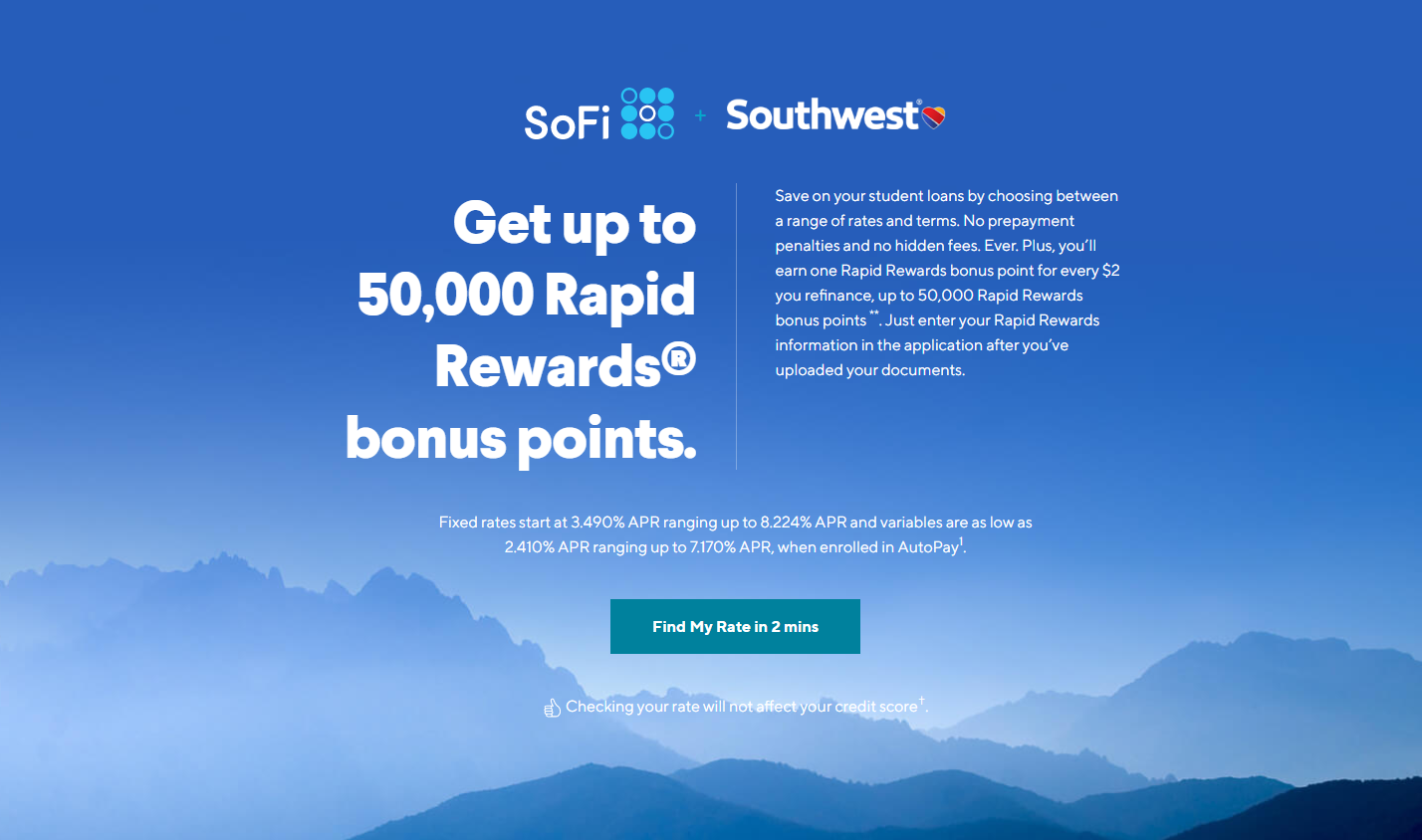

Last week, I received an email from SoFi, offering me 50,000 Rapid Rewards points to refinance my student debt with them. This isn’t the first I’ve seen of SoFi offering miles or points for refinancing, though it is the first time I’ve thought to write up a post, unfortunately.

Refinancing with SoFi

I have to admit, I’ve never refinanced student loans. I’m one of the lucky few that isn’t saddled with a lot of debt. If you guys have any experience refinancing, especially with SoFi, chime in!

On the surface, it looks like you could score a decent deal. Rates are between 2.41% and 8.224% depending on your risk profile. Interest rates are generally low right now, so you should find comparable rates no matter who you refinance your loans with. Keep that in mind, and don’t let those shiny new Rapid Rewards impact your decision too much.

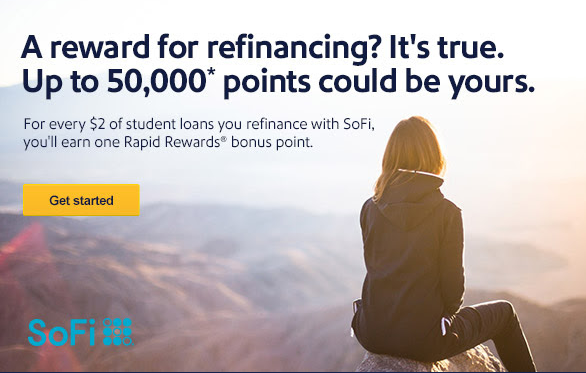

Don’t forget the fine print thought: For every $2 you refinance, you’ll get 1 Rapid Rewards point. That’s a terrible rate! I’ve gotten an average of 1.64 cents per Rapid Rewards point in my few years of redeeming them. That means this offer is worth about a 0.82% one time discount on your total student loan balance.

So, is the SoFi Rapid Rewards deal worth it?

It might be.

But it has nothing to do with those Rapid Rewards. 50,000 Rapid Rewards is worth somewhere between $700 and $900 based on my use of them over the past few years. (Of course, this doesn’t include the much-hyped Southwest Companion Pass.) In the past, I’ve seen offers for TrueBlue points with a SoFi refinancing package, and I think I’ve even seen a United MileagePlus deal too. Plus, you only get that many Rapid Rewards if you refinance $100,000 in student loans! Whoah! Talk about an expensive education.

Here’s the thing: When it comes to debt, virtually the ONLY thing that matters is your interest rate. All other factors constant, your interest rate is the important part. This is the same thing as going with a mortgage lender based on the move-in package they give you – not even remotely worth it, compared to ensuring you get a good interest rate! Who cares about the free toaster?!

No matter what kind of long term debt you have – mortgage, student loans, car note – the interest rate is what impacts your payments, the amount of time you pay, and the total cost over the lifetime of your loan. I’ll leave it to you guys to look up Dave Ramsey on your own.

So, as long as the rate is competitive, and you could use some bonus Rapid Rewards points, go for it! If the rate isn’t good, I’d recommend sticking with whatever loans you have currently, or looking at other student debt consolidation options.

This site is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as thepointsguy.com. This may impact how and where links appear on this site. Responses are not provided or commissioned by the bank advertiser. Some or all of the card offers that appear on the website are from advertisers and that compensation may impact on how and where card products appear on the site. Any opinions expressed in this post are my own, and have not been reviewed, approved, or endorsed by my advertising partners and I do not include all card companies, or all available card offers. Terms apply to American Express benefits and offers and other offers and benefits listed on this page. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. Other links on this page may also pay me a commission - as always, thanks for your support if you use them

User Generated Content Disclosure: Points With a Crew encourages constructive discussions, comments, and questions. Responses are not provided by or commissioned by any bank advertisers. These responses have not been reviewed, approved, or endorsed by the bank advertiser. It is not the responsibility of the bank advertiser to respond to comments.

Dan Miller travels with his wife and 6 (SIX!) children. He loves to help families travel for free / cheap, especially larger families. If you are looking for help, drop him an email at

Dan Miller travels with his wife and 6 (SIX!) children. He loves to help families travel for free / cheap, especially larger families. If you are looking for help, drop him an email at

My brother refinanced his student loans through SoFi and was very satisfied. Said it was easy and interest rate was way better. I didn’t know to refinance so I am only about $4.5k away from paying off at a rate of 6.8%…which isn’t event enough for SoFi to refinance!!

Husband has about $35k left so we’re looking into SoFi since my brother was so pleased.

I hope you guys can snag a good rate too!